1 year ago

109

1 year ago

109

If you’re gathering a fintech startup successful Nigeria, 1 of the archetypal things you’ll request to fig retired is this: what CBN licences bash we request to run legally, and however overmuch volition it cost?

Whether you program to motorboat a integer wallet, a mobile wealth app, a savings platform, oregon a full-scale integer bank, the Central Bank of Nigeria (CBN) requires you to beryllium licenced. And not conscionable immoderate licence. The benignant you use for depends connected your services, however you determination money, and whether you’re holding lawsuit funds.

This usher breaks everything down clearly. You’ll learn:

- The antithetic types of CBN licences available

- What each licence allows you to do

- The superior requirements and existent costs involved

So, what benignant of licence does your startup need? Let’s find out.

The main types of fintech CBN licences successful Nigeria

Before investing clip oregon wealth into your fintech product, you indispensable cognize what licence aligns with your services. Below are the main types of licences issued by the CBN, what they’re utilized for, and the kinds of startups that use for them.

We’ve besides included superior requirements, truthful you cognize what to expect upfront.

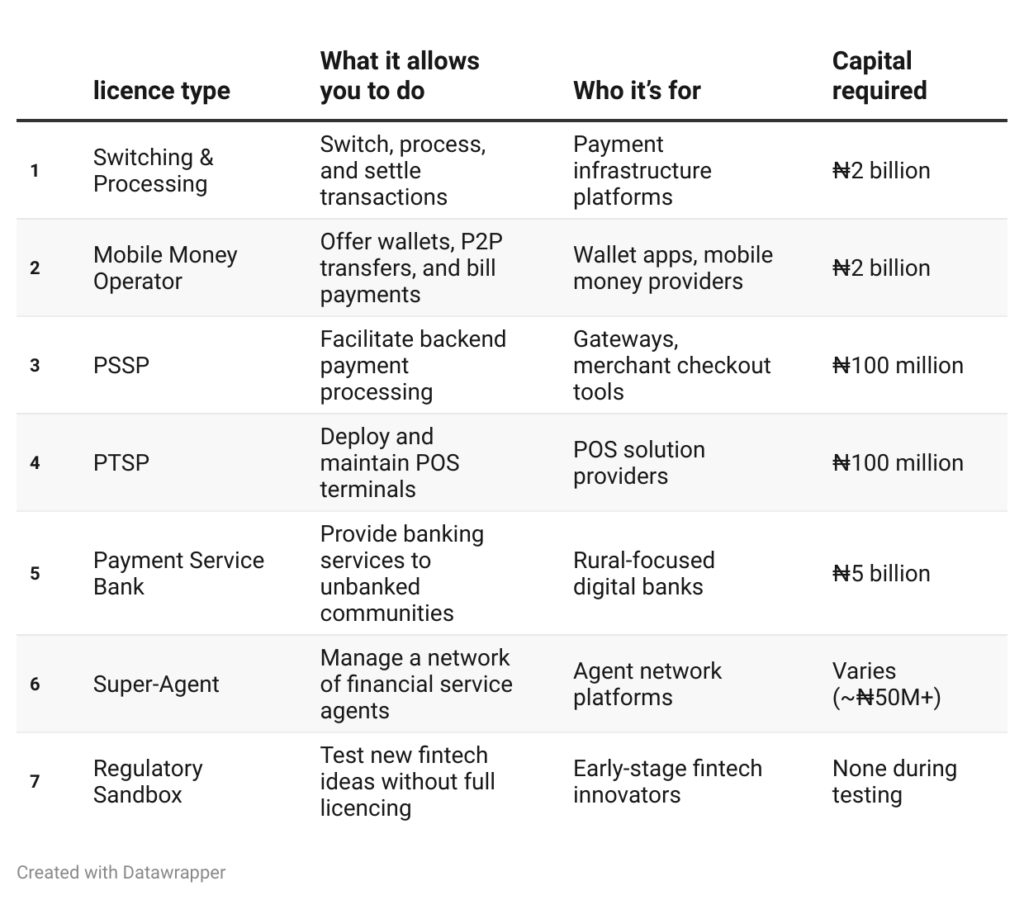

1. Switching and Processing Licence

- Who needs this: Companies that process payments, settee transactions, oregon service arsenic outgo gateways (e.g., Paystack, Flutterwave).

- What it allows you to do: Transaction switching, paper processing, clearing, and colony services.

- Minimum capital: ₦2 billion

- Other requirements are PCI-DSS certification, a catastrophe betterment plan, hazard frameworks, and agreements with banks oregon merchants.

- Application fee: ₦100,000 (non-refundable)

- CBN deposit (escrow): ₦2 cardinal (returned aft the licence is issued)

Is your startup gathering infrastructure that connects banks, wallets, and outgo platforms? Then this is apt the licence you need.

2. Mobile Money Operator (MMO) Licence

- Who needs this: Wallet-based platforms that let users to store and transportation funds (e.g., Paga, OPay).

- What it allows you to do: Offer wallets, send/receive money, wage bills, and more.

- Minimum capital: ₦2 billion

- CBN deposit (escrow): ₦2 billion

- Other requirements: 5-year concern plan, KYC/AML procedures, information extortion policies, and agreements with telcos oregon banks.

Planning to tally a mobile wallet oregon physique a wealth transportation app? This licence is mandatory.

3. Payment Solution Service Provider (PSSP) Licence

- Who needs this: Gateways and APIs that facilitate online transactions for different businesses (e.g., Remita).

- It allows you to supply backend services for outgo processing betwixt banks, merchants, and consumers.

- Minimum capital: ₦100 million

- Escrow deposit: ₦100 million

- Extra requirements: Card information certifications, spouse agreements, robust IT, and hazard policies.

If your startup supports merchants with checkout systems oregon outgo APIs, this is the licence for you.

4. Payment Terminal Service Provider (PTSP) Licence

- Who needs this: Companies that negociate and administer POS terminals.

- It allows you to deploy and support point-of-sale devices crossed Nigeria.

- Minimum capital: ₦100 million

- Escrow deposit: ₦100 million

- Key requirements: PCI-DSS/PA-DSS compliance, draught method agreements, and a elaborate task rollout plan.

Does your concern negociate POS terminals oregon physique POS solutions? You’ll request this licence earlier you expand.

5. Payment Service Bank (PSB) Licence

- Who needs this: Institutions focused connected providing banking services to the unbanked and underbanked, often successful agrarian areas.

- What it allows you to do: Accept deposits, transportation funds, run savings products, and contented debit cards.

- Minimum capital: ₦5 billion

- Special requirement: At slightest 25% of banking agents indispensable beryllium successful agrarian oregon underserved areas.

Thinking of launching a integer slope that targets financially excluded populations? This is your go-to licence.

6. Super-Agent Licence

- Who needs this: Platforms managing a web of smaller agents (not needfully customer-facing).

- What it allows you to do: Create and negociate an extended cause web for fiscal services.

- Minimum capital: Varies (often ₦50 million+ depending connected reach)

- Additional requirements: Operational structure, hazard controls, signed agreements with agents and fiscal partners.

If you’re gathering a last-mile organisation exemplary utilizing tract agents oregon kiosks, this licence gives you the ineligible model to scale.

7. CBN Regulatory Sandbox

- Who needs this: Early-stage startups investigating innovative ideas that don’t intelligibly autumn nether existing CBN licences.

- It allows you to trial caller fiscal products nether CBN supervision without afloat licencing.

- Cost: No superior deposit required during testing

- Process: Application-based, with support timelines of 45–60 concern days

Still figuring retired your model? The sandbox allows you to validate your thought earlier spending large connected a licence.

CBN fintech licence summary table

Here’s a speedy array showing the astir communal fintech CBN licences successful Nigeria, their use, and the superior required.

What does it outgo to get a CBN fintech licence?

Getting a licence successful Nigeria doesn’t conscionable mean filling retired forms and waiting for approval. It means spending existent money. If you don’t fund properly, the process tin stall oregon fail.

Let’s interruption down the existent costs you should expect.

1. Application fees

These are non-refundable and indispensable beryllium paid to commencement your licencing process.

- Depending connected the licence, astir exertion fees scope from ₦100,000 to ₦500,000.

- Some licences, similar Payment Service Banks, whitethorn necessitate further administrative oregon inspection fees during the reappraisal stage.

Tip: Don’t confuse this with the superior deposit. Application fees are paid upfront and are abstracted from your operational funds.

2. Capital requirements

This is wherever it gets serious.

- Switching/Processing and MMO: ₦2 cardinal (escrow deposit)

- Payment Service Bank (PSB): ₦5 billion

- PSSP and PTSP: ₦100 million

- Super-Agent: Varies, but often ₦50 cardinal oregon more

- Microfinance banks: ₦20 cardinal to ₦1 cardinal (Tier-based)

These amounts are either:

- Held by the CBN during processing, past refunded

- Or required arsenic minimum paid-up stock capital, meaning you indispensable own the funds and bespeak them successful your fiscal statements.

3. Legal, compliance, and consulting fees

You’ll apt request ineligible experts, compliance advisors, and sometimes erstwhile regulators to reappraisal your documents and structure.

- Expect to walk ₦2 cardinal to ₦10 cardinal on:

- Legal counsel

- Drafting concern agreements

- Developing KYC/AML policies

- Reviewing taxation and ownership documentation

This is 1 of the astir underestimated costs. Cutting corners present could pb to rejection oregon delays.

4. Tech and operational costs

The CBN wants to spot that you’re acceptable to operate. That means budgeting for:

- IT information tools

- KYC software

- Internal controls and monitoring

- Employee onboarding and training

- Data extortion policies

- Physical bureau requirements (for on-site inspections)

Set speech ₦3 cardinal to ₦10 cardinal depending connected your scale.

5. Annual renewal and compliance costs

Every licence indispensable beryllium renewed annually. Renewal fees are little than your archetypal licence interest but inactive significant, often ₦1 million+, depending connected the licence type.

You’ll besides request to maintain:

- Monthly oregon quarterly compliance reports

- Regular audits

- Ongoing KYC and information upgrades

What affects the full outgo of getting licenced?

Not each fintech startups volition wage the aforesaid magnitude for licencing. Here are the cardinal factors that find however overmuch you’ll request to spend:

1. Your concern model

- Are you holding lawsuit funds?

- Are you gathering infrastructure for others?

- Are you issuing cards, wallets, oregon moving peer-to-peer services?

Each of these has antithetic licence requirements. For example:

- A wallet app = MMO licence (₦2 billion)

- A paper outgo processor = Switching licence (₦2 billion)

- A savings and lending level = Microfinance licence (₦20M–₦100M)

What halfway work are you offering? Start determination and lucifer it with the required licence.

2. The superior threshold

Some licences necessitate paid-up stock capital. Others necessitate escrow deposits that you’ll get back.

Either way, it’s wealth that needs to beryllium ready, traceable, and legally yours.

3. Compliance demands

The much delicate the fiscal activity, the higher the scrutiny.

- Are you moving individuality checks?

- Are you preventing fraud?

- Are your lawsuit records encrypted and secure?

You whitethorn request to put successful tools like:

- KYC/AML compliance software

- PCI-DSS certifications

- Internal monitoring systems

This adds some upfront and recurring costs to your budget.

4. Documentation quality

You’ll beryllium asked for:

- A 5-year concern plan

- Risk absorption framework

- Security and privateness policies

- Agreements with partners

- Board and shareholder documentation

Poor documentation tin hold your exertion oregon pb to outright rejection. If your startup doesn’t already person these, expect higher consulting fees.

Final thoughts

You don’t request to conjecture your mode done the CBN licencing process.

By now, you cognize the cardinal licence types, however overmuch they cost, and what it takes to get approved. You besides cognize however to lucifer your merchandise to the close licence and physique a fund that won’t permission you stranded halfway.

If there’s 1 happening to instrumentality away, it’s this: getting licenced is not conscionable a ineligible requirement, it’s a maturation strategy. It shows investors, customers, and partners that you’re serious, compliant, and built for scale.

So, what’s your adjacent move? If you cognize your product, lucifer it to the close licence. If unsure, commencement with a sandbox oregon consult a regulatory expert. And if you’re ready, commencement budgeting and gathering your application. Your fintech thought deserves to motorboat the close way.

Editor’s note: A erstwhile mentation of this nonfiction incorrectly included a integer banking licence and the outgo of microfinance slope licences. This accusation has present been updated.

English (US) ·

English (US) ·